How Payment Orchestration Increases the Adoption of Open Banking Payments

1. What are the key differences between manual bank transfers and open banking payments?

Manual bank transfers are time-consuming, come with high operational costs and are susceptible to fraud.

Merchants often find themselves sending bank details in a PDF, asking customers to set them up as a payee and then complete payment. In addition to requiring two separate authentications for new payees, customers must input lengthy account numbers, prompting them to carefully double and triple-check to ensure accuracy. The manual nature of the process often results in prolonged back-and-forth within the business, with salespersons coordinating with the finance team to ensure payment completion before goods can be dispatched.

Moreover, sharing bank details in this way is completely insecure because it leaves the door wide open for malicious middlemen to misuse sensitive data. Overall, manual bank transfers are a process rife with serious friction, human error and a heightened risk of fraud.

Enter open banking payments – these are replacing cumbersome bank transfers with an online payment journey. Merchants now have greater control of the process with a “pull payment” rather than forcing the payer to do all the work as a “push payment”. Not only that but it results in faster settlement and quicker access to funds. Merchants enjoy seamless and hassle-free payments directly from their customer’s bank account. Payers no longer need to worry about mistyping account details. With open banking, they simply select their bank, log in to their mobile banking app, and confirm the payment in a familiar setting. Customers authenticate directly from their banking app, and their personal information is encrypted and safeguarded by industry-standard banking security.

In summary, open banking payments are more safe, require less time and manual effort for both merchants and payers, and lead to faster payment settlement.

2. Prommt’s Pay by Bank has seen a 100% increase in adoption rates over the past 6 months. What’s the secret sauce behind this success?

We’re moving from early adoption to the early majority stage of open banking, and because Prommt has been supporting our merchants on that journey for a couple of years we’ve learned a heap about encouraging adoption. I don’t know if there’s a secret sauce but one of the things that Prommt does really well is help merchants orchestrate between open banking and card transactions. Pay by Bank is far more successful when the option to pay by card is also available. Bank is supplementary to card. The success lies in their collaboration, with Pay by Bank proving particularly effective in higher-value transactions. Increasing open banking adoption is not about replacing card transactions altogether.

With Prommt, merchants can set automated thresholds to present their desired payment method, depending on factors like the value, location or transaction type. They can easily set automatic chase paths for failed transactions or where the cart has been abandoned, and present an alternative payment method to complete the transaction – bank or card.

3. Can you delve deeper into how payment orchestration enhances the adoption of Pay by Bank?

Sure, let’s review two client case studies that show how successful Pay by Bank can be through payment orchestration.

Client Case Study 1

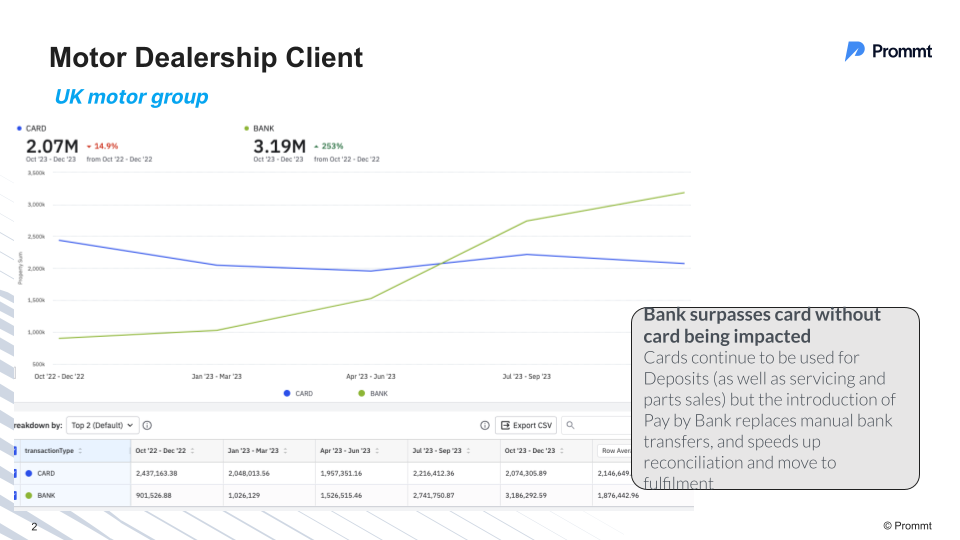

The first example is a large UK motor group, as seen above. They introduced Pay by Bank in Q4 2022 as a way to take on some of their higher value card transactions and their offline bank transfers. They processed around 1 million GBP in their first quarter through Pay by Bank. Over time, they incrementally raised the value threshold. Presently, thanks to Prommt’s payment orchestration controls, any transaction exceeding 5000 GBP is directed straight to Pay by Bank. From processing 1 million GBP in their first quarter to currently processing over 3 million GBP per quarter – that’s a huge success story! Pay by Bank has replaced manual bank transfers, while speeding up reconciliation and move to fulfilment.

Throughout this time, card transactions have stayed consistent between 2 and 2.5 million GBP each month. Pay by Bank has surpassed card without card really being impacted. Card payments are still used for deposits, servicing and parts sales.

Client Case Study 2

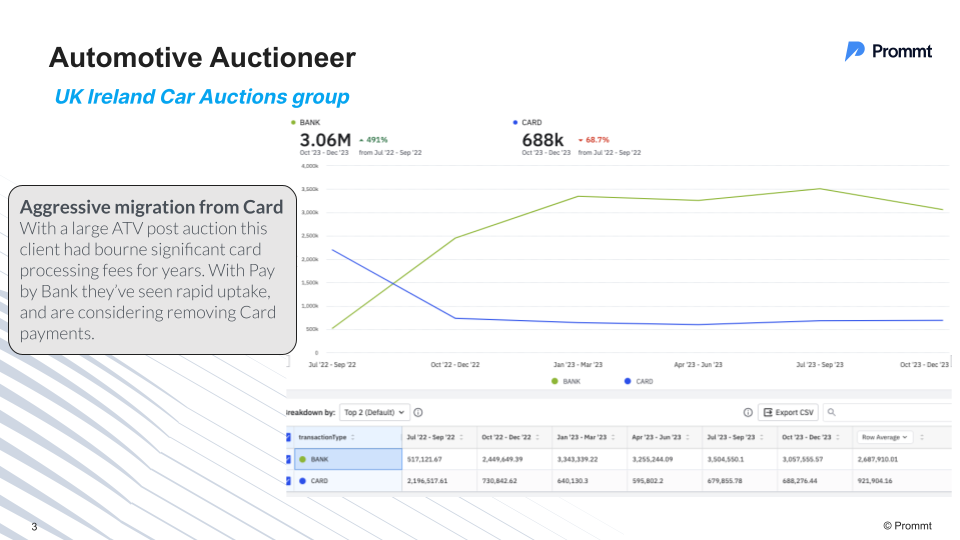

There are some merchants who want to be a bit more aggressive with using Pay by Bank over card, and we can help them in this scenario as well. Our second example is a very large auction company operating in the UK and Ireland, as seen above.

With a high average transaction value post auction, this client had incurred significant card processing fees and operational costs for years before introducing Pay by Bank in Q3 2022. Initially, they were processing about half a million GBP through Pay by Bank and 2 million through card payments per quarter.

And now it has flipped. They’re doing over 3.5 million GBP quarterly through Pay by Bank whilst Card hasn’t gone away as it’s still incredibly important for lower value deposits. With Prommt’s payment orchestration tools they can effortlessly set up automatic value thresholds, gently guiding customers towards their preferred payment method.

4. APP fraud is a real problem on the rise. In the first half of 2023 alone, losses totalling 239.3 million GBP were reported as a direct consequence of these scams. How does Prommt prevent this type of fraud within open banking payments?

Generally Prommt is able to prevent most fraud by providing better context to the payment. It’s something we’ve always been really strong in given our messaging background, and even more so lately with the enhancements we’ve introduced on the back of the guidance from the PSR and Pay.UK.

Typically Automatic Push Payment fraud falls into two buckets:

- ‘Malicious payee’: This happens when people get tricked into buying stuff that doesn’t really exist or never shows up.

- ‘Malicious redirection’: Here, a fraudster pretends to be from the bank and convinces the victim to move money from their account to the scammer’s account.

Prommt prevents malicious payees by conducting comprehensive KYB checks and building strong relationships with our merchant clients. We take onboarding seriously, going beyond the usual routine. It’s a careful process where we make sure all our clients are genuine merchants. We do thorough checks, including KYBC verifications, digging into financial docs, and verifying the backgrounds of owners and directors. It’s all about building a strong foundation, ensuring our clients meet our high standards and share our company values. To keep financial transactions secure, we conduct regular checks on the companies and the bank accounts behind the Prommt clients.

Through the power of context, we boost payer confidence and prevent malicious redirection. Prommt ensures clear and effective merchant-branded communication with payers every step of the way. Payments are managed in the form of a payment conversation, attaching a high degree of context to every transaction. We provide multiple layers of information, including purchase details, bespoke sender IDs, and recognisable URLs. It is crucial that payers fully understand all the steps involved in securely completing a payment, who they are about to pay and why. We also allow the merchant to conduct checks post-payment and pre-fulfilment should malicious activity be flagged. Prommt carefully oversees this interaction to ensure the best outcome for all parties involved.